Designing Your Retirement Paycheck: Turning Savings into Steady Income

For most of your working life, money flows in one direction: from your paycheck into your accounts. You know what hits your bank each month, and you try to save what is left.

Retirement reverses that flow.

Instead of a paycheck funding your savings, your savings now need to fund your paycheck. For many people, that shift, from seeing a “big number” on a statement to understanding how it becomes reliable monthly income, is one of the most stressful parts of retirement.

At On Purpose Financial, we call this “designing your retirement paycheck.” In this article, we will walk through how we help clients turn portfolios into predictable cash flow, protect near-term spending from market swings, and manage taxes more thoughtfully over time.

Seeing your retirement income in three buckets

A helpful way to think about retirement income is as three connected buckets: your everyday checking account, a short term reserve, and your long term portfolio.

Your checking account is where life happens: bills, groceries, and everyday spending. Your portfolio is the collection of accounts you have built over time: 401(k)s, IRAs, Roth IRAs, and taxable investment accounts.

The missing piece for many people is the middle bucket: a reserve that holds roughly one to two years of expected withdrawals in relatively low risk, stable holdings. This middle bucket is what makes your retirement paycheck feel like a paycheck instead of a series of one off transfers.

In practice, the flow looks like this: your portfolio stays invested for your long term goals, we periodically refill the reserve bucket from that portfolio, and your monthly “paycheck” is then pulled from the reserve into your checking account. The money you will need in the next year or two is not riding every market swing; it is already set aside and ready when you need it.

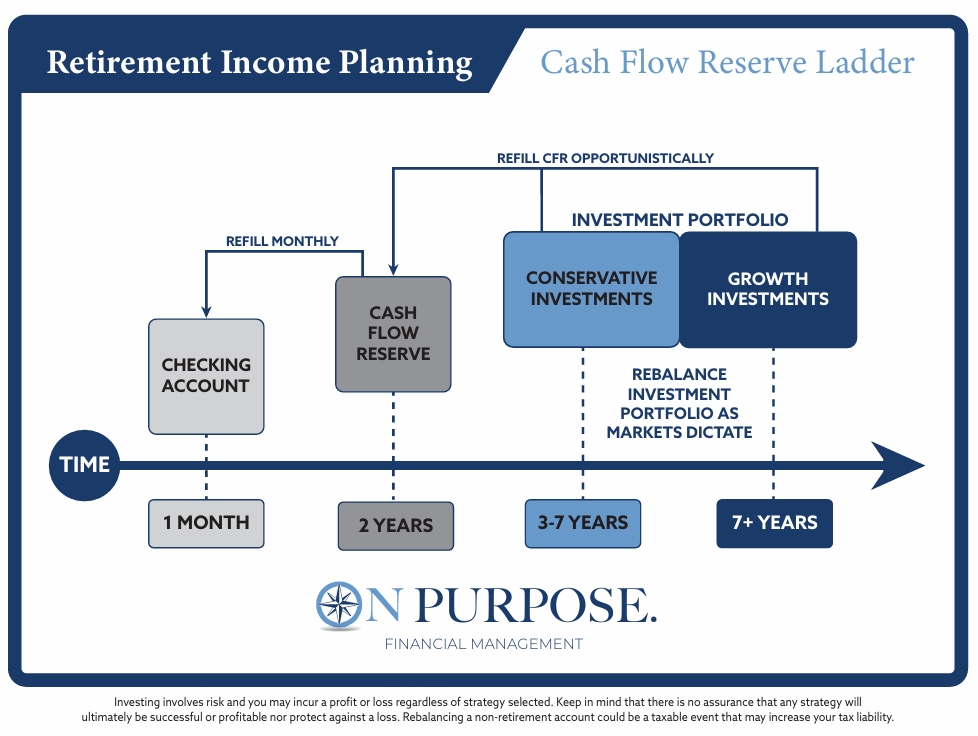

This is exactly what our Cash Flow Reserve Ladder diagram illustrates. On the left is your checking account, in the middle is the cash flow reserve that holds roughly one to two years of spending, and on the right is your investment portfolio divided between conservative and growth investments. Arrows show monthly refills from the reserve to your checking account, and opportunistic refills from your portfolio back into the reserve as markets allow.

Chart: Cash Flow Reserve Ladder

How much belongs in your reserve bucket?

We typically aim to keep about one to two years of planned withdrawals in the reserve bucket. The exact amount is tailored to your situation, but the goal is the same: give you enough cushion that you do not have to sell long term investments in the middle of a downturn just to cover basic expenses.

We usually refill this reserve once a year, not every month. If markets have done well, that can be a good time to trim gains and move some of that growth into the reserve. If markets have struggled, we might let the reserve draw down for a while and wait for a better opportunity to refill from the portfolio.

Will shared a story about clients leading into 2020 and 2022. After strong market years, he noticed that some clients’ cash reserves had dipped below six months of spending. Because portfolios had grown significantly, he recommended topping their reserves back up to a full year or more. Shortly after one of those refills, the pandemic hit and markets fell sharply. Those clients already had a healthy reserve set aside, so they did not need to sell stocks at the bottom to fund their monthly withdrawals. No one predicted COVID; that was not the point. The point was having a consistent process: refilling cash reserves when markets have been kind, instead of waiting for the “gas light” to come on.

Deciding where to pull from

When it is time to refill the reserve, we look across your accounts and ask where it makes the most sense to pull from right now. If the growth portion of your portfolio has done very well, we may take gains there. If growth assets have had a rough patch but more conservative investments have held up better, we may refill from those instead. Sometimes investment income, dividends and interest, flow naturally into the reserve and help keep it topped up.

If everything has been down for a while, we may let the reserve run a bit lower temporarily while we wait for a recovery in at least one part of the portfolio. The goal is to avoid locking in losses unnecessarily.

This is where having a team watching your overall picture can help. When people do this on their own, it is very easy for emotions to creep in, staying invested too long when markets are hot, or selling out of fear when they have already fallen. A disciplined, repeatable process can reduce those emotional whiplashes.

Your retirement paycheck is not just one number

Another key part of designing your retirement paycheck is separating monthly needs from occasional big expenses.

Many new retirees start by saying something like, “I think I will need $100,000 a year.” When we dig in, it often turns out they really need around $6,000 to $7,000 a month for ongoing expenses, plus additional amounts for larger, less frequent items like big trips, car replacements, or major home projects.

We typically encourage clients to set a monthly withdrawal level that covers day to day living and regular bills. Then we plan for larger, irregular expenses separately and fund them when they are actually needed, not by building them into every month’s paycheck.

If extra money arrives in checking every month, it has a way of disappearing, much like closet space that never stays empty for long. By holding back those extra dollars in your portfolio or reserve until you truly need them, you give your money more time to work for you and reduce the chance of “accidental” overspending.

Coordinating with Social Security, pensions, and other income

Your portfolio is rarely the only source of retirement income. Many households also have Social Security benefits, possibly an employer pension, and occasionally income from annuities or other sources.

When we design your retirement paycheck, we first look at what is already coming in automatically, for example, Social Security and any pension checks. Then we calculate the gap between that income and what you want to spend on a monthly basis. Your withdrawals from savings and investments are designed to cover that gap, not the entire budget.

This often means your withdrawal rate looks higher in the early years if you retire before Social Security starts, then drops later once Social Security or a pension kicks in. The structure of your paycheck can change over time, even if your lifestyle does not.

Being thoughtful about taxes

Taxes are a big part of retirement paycheck design. Where your withdrawals come from can change how much you owe.

Some general principles we consider, always in coordination with your tax professional:

- Money taken from a traditional IRA or 401k is typically taxed as ordinary income. Taking too much in a single year can push you into a higher bracket than necessary and also result in higher MediCare premiums.

- Withdrawals from a taxable (non IRA) investment account may create capital gains, which are often taxed at different rates than ordinary income.

- Withdrawals from a Roth IRA, if the rules are met, are generally tax free. This can be a powerful “backup” source for years when you want to avoid pushing your taxable income higher.

- Required Minimum Distributions (RMDs) from traditional IRAs start at a certain age and must be factored into the plan so that you are not surprised by forced taxable withdrawals later.

- If you are charitably inclined, Qualified Charitable Distributions (QCDs) from IRAs, once you are eligible, can allow you to give to charities directly from your IRA without increasing your taxable income, when handled correctly.

Sometimes we even use an IRA as your reserve bucket by creating a separate, very conservative IRA account that holds the next year or two of distributions. The money has been moved out of market risk but is still inside the “IRA bubble,” so you have not triggered taxes until the funds actually leave the IRA system.

We regularly coordinate with clients’ CPAs to help manage how much taxable income is recognized in a given year and from which accounts.

Reverse saving: a mindset shift

During your working years, you save whatever is left after your paycheck covers expenses. In retirement, that flips. You are practicing “reverse saving,” leaving money in place until you truly need it, rather than pulling it out “just in case.”

That means thinking carefully about what you need monthly, identifying which expenses are truly one time or occasional, and letting your investments continue to work for you until it is time to use them.

For many people, having a clear structure, a reserve bucket, a defined monthly withdrawal, and a process for refilling from the portfolio, turns retirement income from a source of anxiety into something that feels as routine as payday used to.

How we help

Designing a retirement paycheck is not just about numbers on a spreadsheet. It is about making your savings feel like a stable, livable income, protecting your near term needs from market volatility, managing taxes thoughtfully over time, and coordinating all of this with Social Security, pensions, healthcare, and your real life.

At On Purpose Financial, we help clients build and maintain this structure so they are not left wondering which account to pull from, how much is “too much,” or whether a market swing should change their entire plan.

If you are approaching retirement, or already in it, and want help turning your savings into a steady paycheck, you can start a conversation with our team at onpurposefinancial.com.

Disclaimer: This article is for educational purposes only and is not tax, legal, or Medicare plan advice. Consult a licensed Medicare professional and your tax advisor for your situation. Material Prepared by Tic Tac Toe Marketing, an independent third party. Any opinions are those of the author, are subject to change without notice and are not necessarily those of Raymond James. This material is being provided for information purposes only and does not purport to be a complete description of the securities, markets, or developments referred to in this material and does not constitute a recommendation. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Investing involves risk and investors may incur a profit or a loss regardless of strategy selected. Neither Raymond James Financial Services nor any Raymond James Financial Advisor renders advice on tax or legal issues, these matters should be discussed with the appropriate professional.